In 1969, when the American Bar Association’s Committee on Ethics and Professional Responsibility first looked at whether a law firm could accept payment via credit cards, they could not have been more disdainful.

The payment of legal fees using credit cards deemed unacceptable. The committee found it was ‘wrong’ to put professional services in the same category as ‘sales of merchandise and sales of nonprofessional services.’ (ABA Committee on Ethics and Prof. Responsibility, informal opn. No. 1120 (1969)).

This opinion set back solo and small law firm finances for the next 50 years.

So, today, do lawyers take credit cards? Even though the opinion was reversed in 1974 (ABA Formal Opinion 338, dated November 16, 1974), lawyers have been slow to accept payment of legal fees from credit cards. In a 2018 survey of law firms by Clio, checks were still the payment method most accepted by firms—44 years after the ABA approved credit card payments. This is in spite of checks being eclipsed by payments being made with credit and debit cards by hundreds of billions of dollars across other industries.

Still, many lawyers are accepting credit card payments—and are getting faster and collecting more because of it. In this article, I’ll take a close look at the ethics of accepting credit card payments for lawyers in every state, some specifics to be aware of, and how to manage them.

Read it through to the end, and you’ll feel secure about ethically accepting credit card payments at your law firm.

Clio Payments give law firms the ability to offer a wide range of legal payment options to clients, including debit, credit, eChecks, tap-to-pay, and direct ACH payments—learn more!

Credit card payments vs check payments: Telling statistics

The US Federal Reserve has tracked payment methods since the year 2000. Checks accounted for nearly $43 billion in transaction value that year. Credit cards and debit cards for only $23.9 billion in that same year. In 2018, the most recent year of published data from the Federal Reserve, checks had declined to $14.5 billion in volume. Credit and debit cards have exploded to $117.4 billion. The use of checks has declined 66%. The use of credit cards has grown 392%!

Law firms not accepting credit cards have cut themselves off from a large pool of consumers.

Why don’t lawyers accept credit cards?

Part of the reason lawyers have not accepted credit cards is that they have very flexible uses. Not every state ethics committee has equally addressed all the issues surrounding this flexibility. Credits cards are just a funds transfer tool. Clients can use credit card charges to pay outstanding invoices, reimburse law firms for expenses, and deposit funds into a firm’s trust account. Lawyers can use charging capabilities to set up payment plans, create flexible billing options, and offer affordable options to clients. Because of these multiple uses, lawyers may need to consider how they are using credit cards before starting to accept them.

In general, there are four ethical questions surrounding the acceptance of credit cards by law firms.

- Can I accept payment for legal fees and expenses via a credit card?

- Can I accept the advance payment of fees via a credit card?

- Can I pass a surcharge to my client to compensate for the processing fees charged by some credit card processors?

- Can I set up recurring charges to customers once they have stored a credit card on file with my law firm?

Firm management software with a built-in payments solution helps you get paid faster—improving your collection rates and firm efficiency. Peggy Gruenke, Law Firm Accounting Specialist at CPN Legal, explains how her Clio Payments can help law firms optimize their cash flow:

In our business, we take care of over 300 Clio clients. The ones that have the best cash flow, spend less time on collecting past due bills, and more time being a lawyer use Clio Payments.

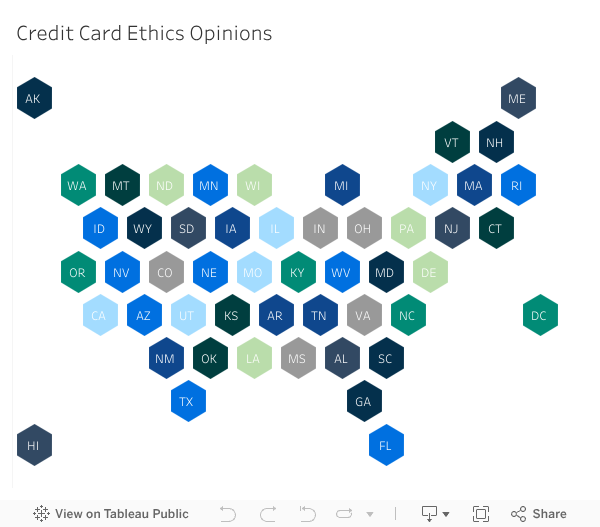

State by state: Ethics opinions on lawyers accepting credit cards

Having researched the ethics opinions for all 50 states and the District of Columbia, you can see the status of your state’s ethical opinions surrounding credit cards here.

- Only four states have issued ethics opinions expressly permitting law firms to accept credit cards in all four of the hypotheticals listed above. Four states have not addressed any of these ethical concerns.

- Ten states have issued ethics opinions on accepting credit cards for fees and expenses, but have not addressed whether a firm can accept credit card transfers as an advanced fee deposit.

- Eight states have ethics opinions forbidding passing credit card surcharges to clients.

So, do lawyers take credit cards?

The short answer is, “yes.” Almost every jurisdiction in the US has come out in favor of law firms accepting credit card payments for legal fees and expenses. Following the American Bar Association’s adoption of the Code of Professional Responsibility (the predecessor to the current Model Rules of Professional Conduct) in 1969, a cascading number of ethics opinions were published throughout the states endorsing the acceptance of credit cards.

At first, these opinions are products of their time. Accepting credit cards was treated as shameful conduct. Lawyers were not able to advertise that they accepted credit cards. For example, lawyers could not display promotional materials provided by a credit card company, ‘‘except possibly a small insignia to be tactfully displayed in the attorney’s office.’ Those Visa and Mastercard stickers on the doors to most retail businesses could not be displayed under these ethics opinions. Nor could firms participate in a directory of firms accepting credit cards.

Fast-forward to today, when Bates v. State Bar of Arizona has changed all that. Freed from many of the constraints on lawyer-advertising, firms can now advertise that they accept credit cards. In states that have not refreshed their ethics opinions on the subject, lawyers may still need to inform their clients about the chance of interest being charged on their payments.

Credit cards, advance fee deposits, and trust accounts

Ethics committees were quick to approve accepting credit cards in payment of legal fees. Those same committees have been slower to approve accepting credit card payments into trust accounts.

There are good reasons to accept advance fee deposits into trust. Clio’s 2017 Legal Trends Report found that firms that accept pre-payment of legal fees into trust accounts have a 18% higher realization rate, and a 15% higher collection rate. Firms that collected fees up front had an average value per case nearly twice that of those that did not.

When advance fee deposits are made via a credit card payment, there does exist the potential for ethical dilemmas.Credit cards have two functions that may impact deposits into trust:

- Chargebacks

- Processing fees

Chargebacks

The first issue when accepting credit card fees into trust is the issue of chargebacks. Lawyers are to hold client-entrusted funds inviolate. No other entity should be able to access funds held in trust.

If a client disputes a charge on their credit card, credit card processors will attempt to claw back money deposited in a disputed transaction. This means the credit card company will be accessing the law firm’s trust account.

Worse, if the funds in dispute have been already transferred, the credit card company may be seizing trust funds that belong to another client. Suddenly the law firm has two angry clients and an ethics complaint brewing.

How to solve

There are a variety of suggestions from ethics committees on how to prevent chargebacks from being an ethical dilemma:

Separate trust accounts:Firms may set up separate trust accounts for clients depositing funds via credit card. Firms may keep funds in trust until not only have they been earned, but the time period in which a client may initiate a chargeback has passed. This varies by credit card provider but is generally around sixty days.

Pull credit card fees from operating accounts. Firms may also contract with credit card processors which have a provision that chargebacks and processing fees are subtracted from an operating account instead. Having such an agreement protects a law firm from having chargebacks creating ethical violations, as the seized funds would not be a client’s but the law firm’s.

Processing fees

The second issue is processing fees. Most credit card processors charge a percentage amount per transaction, subtracting this amount from the net total deposited to the merchant. Most charge between 2-3% of a transaction. A client may deposit $1,000 into their law firm’s trust account. The lawyer receives only $980 to deposit into trust. Twenty dollars has been collected as a processing fee. This could create ethical issues if the client was relying on the full total being available for bills or expenses related to their matter.

How to solve

An attorney can skirt this problem by covering the cost of the processing fee themselves or passing a surcharge for the amount to their client.

For more tips on credit cards, additional fees, and online payments for lawyers, visit our payments resource hub.

Who pays credit card processing fees in legal billing? Charging for charging.

It is ethical in some jurisdictions for lawyers to pass on credit card processing fees to clients, but overall, it is not recommended. A reversal of previous ethics opinions has happened. It is better to accept these fees as the cost of doing business.

Processing fees may not seem significant when they are part of small purchases. 2% of the purchase price of a candy bar does not feel big. 2% of a $10,000 bill will definitely feel significant. (It is not significant. 2% of $10,000 is only $200.)

Aside from ethical issues, processing fees are probably the biggest reason lawyers have avoided accepting credit cards.

In jurisdictions that have adopted the language in the ABA’s 1974 ethics opinion permitting credit card payments, passing along surcharges may not be allowed.

The original language reads,

4. A lawyer shall not encourage participation in the plan, but his position must be that he accepts the plan as a convenience for clients who desire it; and the lawyer may not because of his participation increase his fee for legal services rendered to the client.

5. Charges made by lawyers to clients pursuant to a credit card plan shall be only for services actually rendered or cash actually paid on behalf of a client.

If your jurisdiction’s current ethics opinion contains this language, passing a surcharge onto your client may be an ethical violation. A charge would be either an increase in fees different than those paid by other means, or a charge for something other than fees or cash paid by a client. In either case, a surcharge is not ethical.

Other states, like Connecticut, expressly forbid surcharges. Lawyers are to treat credit card processing fees as ‘as an overhead cost or ordinary cost of doing business.’ When depositing advance payments into trust, law firms in that state must immediately deposit their own funds into the trust account to cover any charges that may have been incurred and deducted from the client’s payment.

Some states expressly permit passable surcharges for credit card fees. If a law firm is passing along the fees, Lawyers should notify their client as part of their written engagement letter or fee agreement that these charges will be imposed. Clients need to know what will be the basis for calculating these charges. In order for a charge to be reasonable, it should be no more than the actual processing fee amount.

Even in jurisdictions where passable surcharges are allowed, many ethics opinions recommend not imposing them. A reversal of previous ethics opinions has happened. It is now considered mercantile to chase after credit card fees. Just accept the fees as part of doing business, as these opinions urge.

Using client credit card data for recurring charges

Once a client has paid one invoice or trust deposit with a credit card, may the law firm continue to add new charges to the card? Eight states have ethics opinions that expressly permit recurring charges. No state has an ethics opinion forbidding repeating charges.

Some of these ethics opinions envision a lawyer imposing time limits for paying invoices. When the time limit is exceeded, the lawyer would like to charge the client’s credit card for the outstanding amount. Others simply anticipate automatic charges when bills are issued. In each of these opinions, advanced notice to the client is necessary at multiple times.

Clients should be notified when the credit card number is collected that it may be used for additional charges. Clients should also be notified prior to an additional charge being levied.

The basis for the second notice is to allow the client to make payment arrangements with different funds. A client’s economic situation may not support unanticipated payments coming from a debit card or credit card. Lawyers should be mindful of the client’s circumstances and let clients decide if the charge should continue.

Payment plans are one form of recurring credit card charges that can be useful for many law firms. Clio Payments has payment plans built in. Give your clients more flexibility with customized payment plans. Break large bills into manageable amounts on a schedule that fits their needs—helping you collect more of your outstanding balances. Clio’s Legal Trends research has found that 72% of consumers would prefer to pay their legal fees via payment plans.

What if my state has no applicable ethics opinion?

Do not assume that a lack of ethics opinions in your state means that you cannot accept credit cards. Every state in the US has adopted the ABA’s Model Rules of Professional Conduct. Most states have an ethical analysis that is intentionally similar to others reviewing the same rules. Citations to external jurisdiction’s approaches are common as supporting evidence for the opinion’s conclusions. If your state does not have an explicit ethics opinion, look to neighboring jurisdictions.

It is important to mention that most states’ rules are broadly permissive. When something is not permitted, such guidance is narrowly tailored to very specific actions. An absence of guidance is not evidence of an action being unethical. Lawyers can proceed with credit cards, provided they follow the Rules of Professional Conduct as written in their state. If you still feel a use case may be questionable, reach out to ethics hotlines available to you for direct guidance.

Compliance with credits cards beyond ethics opinions

Accepting credit cards is not just an ethical issue, but also a compliance one. Businesses accepting credit cards are asked to comply with the Payment Card Industry (PCI) standards put forth by major processors. For businesses accepting credit card payments, there are five compliance goals suggested by the industry:

- Build and maintain a secure network.

- Protect Cardholder Data.

- Maintain a Vulnerability Management Program.

- Implement Strong Access Control Measures.

- Maintain an Information Security Policy.

By using Clio Payments, law firms can speed up recurring payments by storing client payment information in compliance with PCI standards. Clio uses the payment industry’s most advanced security measures—with bank-grade protection of your client’s data and proactive fraud detection—so you can safely accept online payments and store card details for future transactions.

Electronic payments are a permanent fixture for law firms

Despite a late start, 53% of law firms are new equipped to accept electronic payments. Consumers adoption of electronic payment methods is finally starting to penetrate the legal industry. Mostly this is due to client demand. Clio’s Legal Trends research shows that 50% of clients are more likely to hire a lawyer who takes electronic payments, 47% are more likely to hire a lawyer who accepts automated payments or fund transfers, and 40% would never hire a lawyer who didn’t take credit or debit cards.

Accepting credit and debit cards (along with other online payments like eChecks, and direct ACH payments) as payment sources will enhance your law firm’s collection rate, and ability to attract paying customers. If ethical concerns have been preventing you from accepting credit card payments, use this guide to determine where your state stands and begin moving your firm’s billing into the modern age.

Clio Payments aids law firms in providing payment flexibility to their clients, such as online payments, automated payment reminders, bulk billing, and split billing functionality to allow for multiple payers. Book a demo today and learn all about Clio Payments’ powerful capabilities.

Note: The information in this article applies only to US practices. This post is provided for informational purposes only. It does not constitute legal, business, or accounting advice.

Subscribe to the blog

-

Software made for law firms, loved by clients

We're the world's leading provider of cloud-based legal software. With Clio's low-barrier and affordable solutions, lawyers can manage and grow their firms more effectively, more profitably, and with better client experiences. We're redefining how lawyers manage their firms by equipping them with essential tools to run their firms securely from any device, anywhere.

Learn More